SaaS Disruption and the AI Tax: Salesforce’s Toll-Road Strategy

How AI platforms could commoditise SaaS — and why winners must become destinations for agentic traffic.

Historically, the economics of SaaS companies were underpinned by direct, subscription-based relationships with their customers. That relationship is now under threat.

AI model companies such as OpenAI and Anthropic are no longer just infrastructure providers. They now have their own applications, rapidly growing user bases and unprecedented access to capital. OpenAI’s ChatGPT has over 900m weekly active users, while OpenAI’s latest financing round included $122bn of committed capital — a sum larger than the market value of many leading SaaS companies. Directly contesting that distribution is no longer realistic for most companies.

Over twenty years ago, Google turned newspapers into commoditised suppliers competing for distribution. AI model companies could do the same to SaaS — capture the “eyeballs” where enterprise work begins, make SaaS apps compete for distribution, and extract an “AI Tax” through inference costs and weaker customer access.

The emerging split is between SaaS companies that become preferred destinations for agentic traffic, and those that must pay to attract it. For investors, the question is whether a company can build the infrastructure required to capture that traffic—and turn it into revenue.

In this article, I break down:

How SaaS applications with authoritative data are building “toll roads” for agentic traffic.

How leading incumbents are developing pricing models that scale beyond commoditised data access.

How these companies have deployed billions in acquisitions over the past 18 months alone to build this defensive infrastructure.

Salesforce appears to have shown the clearest awareness of this shift. Its AI infrastructure has been more expansive than its peers, and it began early with integration platform MuleSoft in 2018. If MuleSoft’s integration advantage compounds over time, that early bet may become Salesforce’s most important strategic advantage. While my experience as a Salesforce shareholder has been tumultuous, I’m holding onto my position.*

*All opinions are personal. This is NOT investment advice. Please do your own research and seek professional advice

Losing the Engagement Layer

“… These new models, whether it’s OpenAI, whether it’s Anthropic, whether it’s Gemini … are new parts of our infrastructure that we really did not have in place a few years ago…there’s thousands of them … we’ve always had models at the bottom of our infrastructure.” Marc Benioff, Salesforce founder and CEO, at the Salesforce earnings call in February 2026.

Unsurprisingly, Benioff describes a world where AI models, such as Anthropic’s Claude, are commoditised. Value continues to be captured by Salesforce’s applications, positioned above the model layer.

Chart 1: Salesforce’s ideal agentic architecture, where SaaS applications sit above a commoditised model layer

Benioff’s position is understandable. Traditional SaaS enjoyed exceptional economics because revenue scaled faster than usage costs. Subscription pricing was predictable, while the marginal cost of serving heavier users was minimal. That meant vendors could encourage deeper engagement without sacrificing gross margin. In fact, the heaviest users were often the most valuable: they drove retention, seat expansion, pricing power and net revenue retention.

But Benioff’s diagram depends on a second, more fragile assumption: that Salesforce maintains its direct relationship with its users.

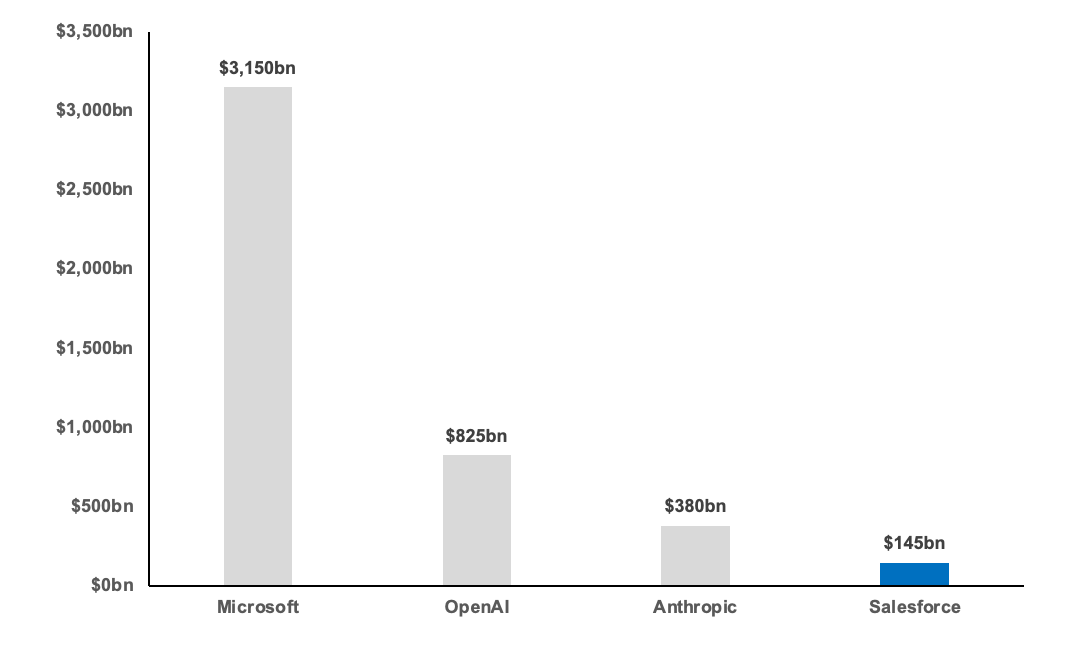

The problem for Salesforce is that the AI model companies have their own enterprise applications, where users are rapidly gathering and AI agents are being created. ChatGPT took just three years to exceed 700 million weekly active users and already exceeds Slack’s userbase by an order of magnitude. While it is not an AI model company, Microsoft’s Teams application sits on every enterprise desktop via Microsoft 365 bundling. Claude is on a similar trajectory. The capital backing of each is an order of magnitude larger than Salesforce’s.

Chart 2: Microsoft, OpenAI and Anthropic have significantly more access to capital than Salesforce

Unless you’re Microsoft, winning the engagement layer is not a fight SaaS companies will want to engage in. Recent SaaS partnerships with model companies show that management teams are increasingly conceding the point. That is where the pressure on SaaS economics begins.

The AI Tax on SaaS Margins

“...our fundamental goal is to be where the eyeballs are. We want all of our platform capabilities to be where customers are…” — Sasan Goodarzi, Intuit Chairman & CEO, Q2 FY26 earnings call.

Intuit’s arrangement with Anthropic is one of many similar partnerships being announced by SaaS companies. The deal allows Intuit to use Anthropic’s models inside its software, in exchange for allowing Claude users to access Intuit’s services inside Claude.

The analyst pushback is understandable. Making TurboTax available inside Claude concedes that customer intent — the “eyeballs” — is moving to AI platforms. Once there, TurboTax competes for distribution on the platform’s terms, much like consumer brands inside Amazon. The result is brand commoditisation and reduced pricing power.

This is the first part of the AI Tax: SaaS companies lose some control over distribution, brand presentation and pricing when customer intent moves to AI platforms.

Chart 3: SaaS applications risk commoditisation as they compete for distribution on AI model company applications

The second part is more direct: inference cost.

“And from an economic perspective, we own the experience and the relationship and we don’t share in the economics while at the same time we’ve committed to continued use of external LLMs, which is part of the Anthropic deal.” Sasan Goodarzi, Intuit Chairman & CEO, 2Q26 earnings call.

Goodarzi’s claim is technically correct: the model companies do not take a direct cut of Intuit’s revenue. It is also irrelevant. The model companies do not need a take rate to extract Intuit’s rent — they charge for it directly, through inference fees.

As SaaS companies build AI features into their products, every Claude or GPT call those features make, is paid for by the SaaS vendor as inference fees at a price the model companies control. This is a variable cost scaling with usage, a stark departure from the low marginal cost environment long enjoyed by SaaS companies. Jason Lemkin, founder of SaaStr, cited data from ICONIQ’s State of AI report that showed inference costs averaging 23% of total AI product costs at B2B companies even as they scale.

The old SaaS bargain is breaking down. Heavy users used to be the best customers because they drove retention and expansion without adding much cost. They are now the most expensive to serve —the cohort that defined the SaaS investment case now defines the margin risk.

Chart 4: SaaS companies face an AI “tax” from brand commoditisation and inference costs paid to AI model companies

With competitors aggressively promoting AI enabled features, cutting inference cost is not an option. Enterprise AI budgets have exploded while overall IT budgets have not. Lemkin frames this competitive dynamic most directly:

“The “AI agents replace SaaS” thesis is lazy … SaaS is being starved, not killed” Jason Lemkin, SaaStr Founder, early 2026.

Not every SaaS company is equally exposed. The winners will be those that make their platforms a destination for AI agents — the place agents go to access trusted data, apply business context and complete customer workflows. These are the building blocks to turn agentic usage into revenue.

Building the Agentic Toll Road

Salesforce, Workday and Intuit share one important advantage. They are systems of record — meaning their data is the authoritative source of truth in their category. Salesforce holds customer and pipeline data. Workday holds employee and payroll data. Intuit’s QuickBooks holds the financial records for millions of small and mid-market businesses.

Agents need more than AI models. To complete work, they need trusted data, business context and permission to act. These are ingredients that systems of record already possess.

This gives systems of record a natural role as toll roads for agentic workflows. If an agent needs to update a customer record, approve a payroll change, reconcile an invoice or trigger a service workflow, it usually must pass through the authoritative system. That creates a path to turn AI usage into revenue, rather than simply absorbing AI costs.

Workday’s Gerrit Kazmaier described this emerging pricing model on the company’s Q4 FY26 earnings call:

“…we have a tiered pricing structure for AI or programmatic access to the Workday platform … we capture consumption in the form of API calls … this is the most basic unit. Data cloud … is available on Flex Credits. It provides richer context. And if third parties want to aggregate agents … they have a premium price tag to them … because they complete meaningful work.“ Gerrit Kazmaier, Workday President of Product & Technology, Q4 FY26 earnings call, February 2026.

Kazmaier’s comments imply a simple pricing ladder: reading data, understanding context and completing work. Pricing power increases at each step.

Data access is the foundation, but it is also the easiest tier to commoditise. The larger prize is action, where customers pay for labour avoided and work completed.

Chart 5: Systems of record are leveraging their data advantages to create a three-tier usage based pricing structure linked to customer outcomes

That is why the moat is not the API call itself. The moat is the infrastructure behind it: trusted data, integration depth, governance and workflow execution. The systems of record that have been building the infrastructure around their data are best positioned to capture value across all three tiers.

MCP Is the Toll Booth; MuleSoft Is the Road Network

“Salesforce has launched a new product that lets its customers connect other companies’ AI agents with their Salesforce data ... known as a hosted Model Context Protocol server, which suggests that it is exploring ways to generate revenue from customers using outside AI agents, following similar moves by rivals such as ServiceNow and Workday.” Laura Bratton, Reporter at The Information, April 2026.

The pricing model described in the previous section is already being implemented. Salesforce, ServiceNow and Workday are launching hosted Model Context Protocol (MCP) servers — effectively toll booths that let AI agents connect to and be charged for using enterprise software systems.

However, a toll booth is only as valuable as the road it sits on. An AI agent may route around a toll if it can find the same data elsewhere, resulting in lost revenue. The larger question is whether Salesforce can make itself the road that agents prefer to use.

Chart 6: SaaS companies only monetise agentic traffic that flows through their own MCP Toll-Booth

Salesforce’s system-of-record position gives it a starting point. Agents that need trusted customer, sales or service data will still need to access Salesforce. But the larger prize is workflow execution — helping agents complete work, not just retrieve records.

As ServiceNow CFO Gina Mastantuono puts it:

“Customers aren’t paying us for tokens. They’re paying for a resolved outcome. Reasoning is one input. Workflow orchestration, governance, context, cross-system action, that’s where the other 90% of the value and costs sit.” Gina M. Mastantuono, ServiceNow President & CFO, ServiceNow Analyst Day, May 2026

That is the right economic framing. The value sits in resolved outcomes, not model usage.

Salesforce’s advantage is focus. It does not need to orchestrate every enterprise workflow. It can focus on customer-facing work — sales, service, marketing, account research and customer success — where it already has the data, user relationships and workflow history.

MuleSoft makes Salesforce harder to bypass by connecting its CRM data to the other systems where customer workflows occur. Acquired in 2018 for $6.5bn, MuleSoft is the integration layer that connects Salesforce to the rest of the customer’s IT systems. That matters because real enterprise workflows rarely sit inside one application. A sales agent preparing for a major customer meeting may need Salesforce data on the prospect, Workday data on internal experts, product usage data from another system and contract data from finance.

Without MuleSoft, Salesforce may capture only the CRM data call while the broader workflow is orchestrated elsewhere. With MuleSoft, Salesforce has a better chance of keeping the workflow inside its own infrastructure and capturing the workflow premium.

Chart 7: MuleSoft’s deep integrations make Salesforce a natural destination for agentic workflows.

This is the core of the Salesforce advantage. MCP gives Salesforce a toll booth. MuleSoft gives it a road network. The more systems MuleSoft connects, the more useful that network becomes for customers, developers and agents. Because those network effects compound over time, MuleSoft’s position is difficult to replicate with capital alone.

Recent acquisitions in data governance, including Informatica and Own Company, extend its infrastructure further. But MuleSoft remains the key asset. It gives Salesforce a path to monetise not just access to CRM data, but higher-value workflows that move across enterprise systems.

Salesforce bought that integration network years before AI agents made cross-system workflows strategically important. That buildout was expensive, which is the focus of the next section.

The New Cost of Defensibility

“So I think we’re now in the action phase of AI, where it’s not a proof of concept. It’s not just a game where I can push information and summaries at you. Someone’s got to be able to put that in a formative way so decisions can be made from it.” William McDermott, ServiceNow CEO, Citizens JMP Technology Conference, March 2026.

McDermott’s comments capture where SaaS AI is heading. The proof-of-concept phase is over; the buildout phase is underway. Companies that want to monetise agentic workflows need more than model access. They need infrastructure that makes their platforms natural destinations for agents, not just applications waiting to be queried.

That infrastructure is expensive.

ServiceNow has completed roughly $12bn of major AI-related acquisitions in 2026. Workday closed around $2bn of transactions in 2025. Salesforce’s capital deployment has been larger and earlier: $44bn of total acquisitions, or $16bn excluding Slack, beginning with MuleSoft in 2018.

Chart 8: Salesforce has led SaaS companies in a multi-billion dollar AI acquisition spree beginning in 2018

Capital spend does not automatically create a moat. The relevant question is not how much a company has spent, but whether the spend makes its platform more useful to agents, harder to bypass, and easier to monetise. The early signals are notable. Salesforce’s Agentforce reached $800m in annualised recurring revenue, ServiceNow expects $1.5bn in annual commitments for Now Assist by the end of 2026, and Workday estimates $400m in ARR from AI-related solutions. The figures remain small against each company’s revenue base, but the strategic focus is clear.

The contrast with growth-focused SaaS peers is sharp. Intuit’s $12bn acquisition of Mailchimp and Xero’s $2.5bn acquisition of Melio Payments were focused on TAM expansion rather than AI workflow infrastructure. While their management teams would have had their justifications, they do highlight the strategic divide: some SaaS companies are buying growth adjacency, while others are assembling the infrastructure required to monetise agentic workflows.

The warning for investors is straightforward. Defensible AI is not just a product feature, it is becoming an infrastructure problem. Companies that have not yet invested in integration, governance and orchestration may be starting from behind in a race where delays are costly.

The SaaS Underwriting Test

As enterprise users begin work inside platforms like ChatGPT and Claude, SaaS companies face margin pressure from increased competition, brand commoditisation and inference costs paid to model companies.

The emerging split is between SaaS companies that become destinations for agentic traffic and those that must pay to attract it. The investment question is whether a company can become the preferred destination for agentic traffic — and turn that traffic into revenue. Investors should focus on three tests:

Data advantage: AI agents need accurate, current data. Systems of record like Salesforce should continue to attract traffic in their core domains because they hold the authoritative customer record.

AI infrastructure: Data access is necessary but not sufficient. The larger prize is workflow execution — helping agents apply context, move across systems and complete customer outcomes.

Capital intensity: Building this infrastructure is expensive. Major SaaS companies have invested billions in the last 18 months alone. SaaS companies that have not made the necessary investments may be starting from behind.

A toll-booth on one road only collects what crosses that road. Salesforce’s advantage is that it may own both the toll-booth and enough of the surrounding road network to capture higher-value agentic workflows. Whether by founder-led vision or good timing, Salesforce began building that network early. If MuleSoft’s integration advantage compounds over time, that early bet may become Salesforce’s most important strategic advantage.

Chart 9: Salesforce bet early and big with its AI infrastructure buildout

Venture Journeys articles are provided for informational purposes only and should not be construed as investment, business, legal or tax advice. Please do your own research or consult advisors on these subjects.